Recession Warning? U.S. Consumer Debt Surges to $16.9 Trillion As Debt Delinquencies Soar

Consumer debt doubled compared to pre-pandemic levels as inflation continues to persist and remains at its highest levels in 40 years, despite multiple aggressive interest rate increases.

The Federal Reserve is reporting that consumer debt continues to increase as more consumers fall behind on their monthly payments. This is yet another red flag indicating that a recession is not a remote possibility.

According to the Federal Reserve, consumer debt grew by $15.3 billion, approximately a 4% annual increase, in February 2023. This has become a trend as January 2023 saw an increase of $19.5 billion dollars in consumer debt. As of the end of the first quarter of 2023, American consumer debt reached a record high of $4.8 trillion dollars. As Americans struggle with inflated prices and economic uncertainty, they keep pilling on debt, primarily credit card debt, in order to make ends meet.

Consumer debt is this umbrella term that includes credit card debt, which typically accounts for its the biggest portion, as well as student loans, vehicle loans and a variety of personal loans. Consumer debt excludes mortgage debt but when combined, it becomes clear that there is no easy solution to the problem: American consumes owe approximately $17 trillion dollars in debt.

According to Experian, average consumer debt levels increased by 7% in 2022, which represents the largest increase in household debt in two decades. To put the numbers into perspective, the annual increase was 3.6% in 2019. Consumer debt has nearly doubled compared to pre-pandemic levels as inflation continues to persist and remains at its highest levels in 40 years.

Climbing consumer debt and inflation, in addition to rising interest rates, paint a grim forecast. Due to the fact that inflation persists, the Federal Reserve is expected to continue hiking interest rates. While this may bring the desired - for the Fed- outcome of somehow controlling inflation (i.e. the inflation the Fed allowed to get out of control), it will undeniably cause more pain to average consumers who typically do not have multiple streams of income and are already struggling to keep up with their monthly bills and other unavoidable expenses.

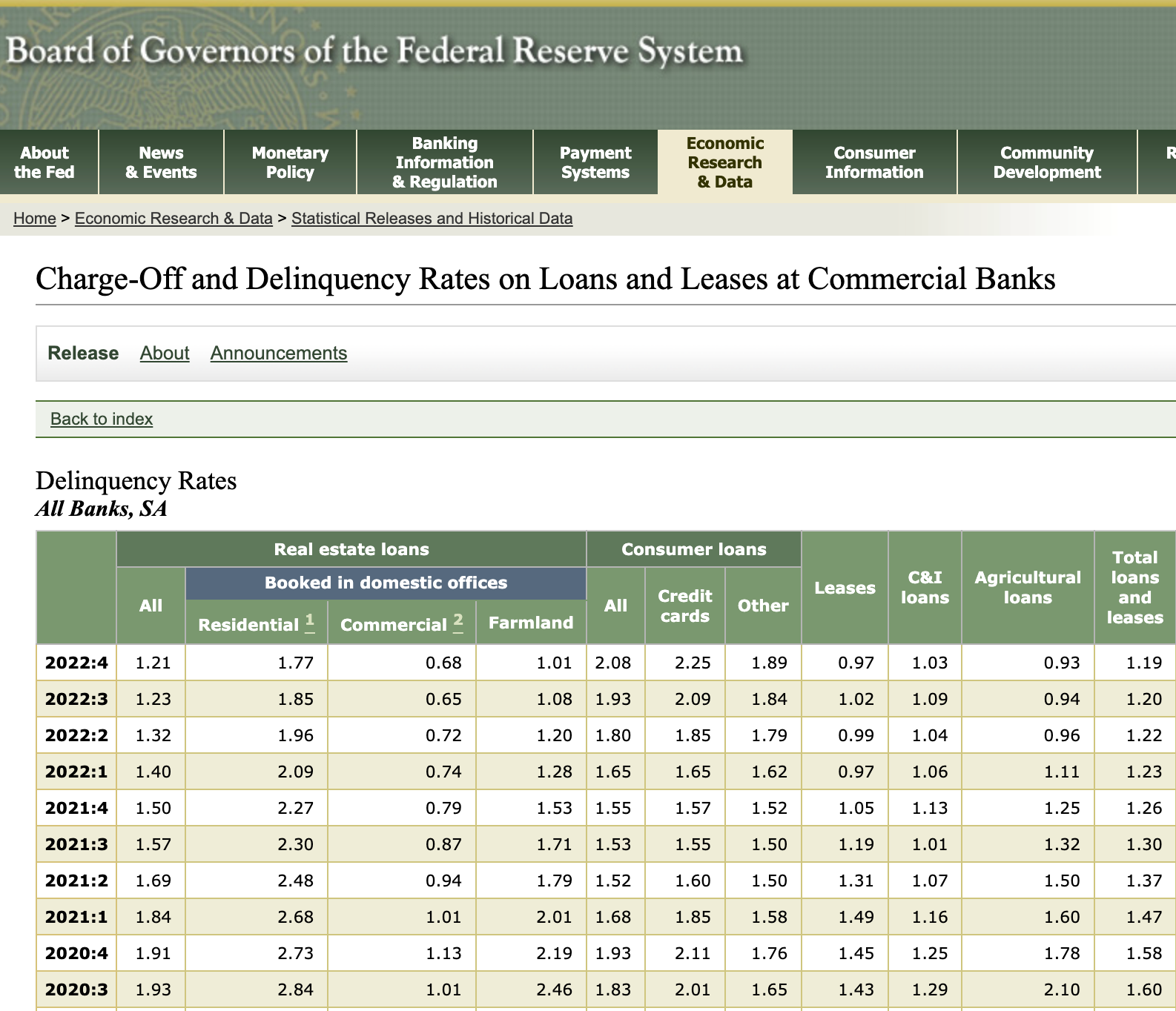

Consumers are struggling to make monthly payments. The data of this nature is reported through delinquency rates that are said to be rising and are currently at levels not seen since 2008-2009. Based on the data announced by the Federal Reserve, mortgages, auto loans and credit card delinquencies are increasing.

Mortgage loans considered in “serious delinquency” of 90 days or more rose to a rate of 0.57%, still low but nearly double where they were from the year prior. Auto loan debt delinquencies rose 0.6 percentage point to 2.2%, while credit card debt jumped 0.8 percentage point to 4%. (Federal Bank of New York)

Charge off and delinquency rates have been rising since the beginning of 2022:

Consumer debt has been steadily rising. Experian reported that in 2022, consumer debt grew across the board, including mortgage and home equity loans increasing approximately 10%; auto loans increased by 6%,; credit card debt went up 16%, and personal loans increased 18%.

The latest consumer debt data shows that consumer debt continues to grow but at a slower pace. According to Experian, significant increases in consumer debt was irrespective of someone’s income, credit score or age.

Additionally, non revolving credit numbers (ie. term loans such as vehicle loans, student loans, mortgages, etc.) have dropped while credit card debt is surging. It points to the U.S. economy slowing down due to high interest rates and wages not keeping up with the increase in prices. Consumers are cutting back on “large” items while resorting to financing routine purchases, such as groceries. The trend is indicative of the fact that due to the fact that credit card debt is growing, consumers may be approaching their credit card limits and, as the result, are indirectly forced to cut back on their spending.

If the assumption that consumer debt growth is slowing as the result of consumers approaching their debt limits is accurate, we should ask ourselves: “What happens next? Is this going to result in higher rates of delinquencies? If so, coupled with increasing interest rates, just how bad will it get?”

The tile of the article should be , Deprecation Warning ,China the second largest holder of of U.S. debt

behind Japan at @ 860 billion dollars is now dumping their dollar assets, preparing for War , and Japan has switched to the East , purchasing Russian energy and away from the U.S.

What will the U.S. do when all imports to the U.S stop ???

Vlad