Japan’s Bond Market Shock Is Triggering a New U.S. Debt Crisis

For many decades, the United States benefited from an extraordinary financial privilege. Washington could run enormous budget deficits, issue vast quantities of Treasury bonds, and still rely on steady global demand for its debt. Foreign governments, pension funds, insurance companies, and institutional investors consistently purchased U.S. Treasuries because they were considered the safest and most liquid assets in the international financial system. At the center of this arrangement stood the U.S. dollar’s role as the world’s reserve currency.

Yet a potentially historic shift is now emerging inside the global bond market. One of the largest and most important foreign buyers of U.S. debt — Japan — may be beginning to pull capital back home. If this trend accelerates, the consequences for U.S. borrowing costs, financial markets, and the broader global economy could become profound.

Japanese investors collectively hold approximately $1 trillion in U.S. Treasury securities, making Japan the single largest foreign holder of American debt.

Japanese capital flowed into U.S. financial markets because domestic investment opportunities inside Japan were extraordinarily limited. Following the collapse of Japan’s asset bubble in the early 1990s, the country entered a prolonged period of stagnation, weak growth, and deflation. In response, the Bank of Japan implemented some of the most aggressive monetary easing policies in modern history.

Interest rates in Japan remained near zero for years, and at times even turned negative. Japanese government bonds offered such low yields that large institutional investors increasingly searched abroad for higher returns. Pension funds, insurance companies, and asset managers shifted enormous quantities of capital into overseas markets, particularly the United States, where Treasury bonds and corporate debt offered substantially higher yields.

This dynamic became one of the foundational pillars supporting the modern U.S. debt market. Foreign capital inflows helped finance expanding American deficits while keeping borrowing costs relatively manageable. As long as foreign demand for Treasuries remained strong, Washington could continue issuing debt at comparatively low interest rates.

That environment, however, is beginning to change.

Japan’s financial system is undergoing a historic transformation as inflation returns after decades of persistent deflationary pressure. Rising energy costs, supply-chain disruptions, and broader global inflationary trends have forced Japanese policymakers to abandon many of the ultra-loose monetary policies that defined the past three decades.

The Bank of Japan has already raised interest rates to levels not seen in decades and is widely expected to tighten policy further in the coming months. Markets increasingly anticipate another rate increase that could raise Japan’s benchmark interest rate from 0.75% to 1%. Although these figures may appear modest by American standards, for Japan, they represent a dramatic policy reversal.

The implications for Japan’s bond market have been substantial. Yields on Japanese government bonds (JGBs) have surged sharply across the maturity spectrum. The benchmark 10-year Japanese government bond recently climbed to approximately 2.73 percent, its highest level since 1997. Meanwhile, the yield on the 30-year JGB reached 4 percent for the first time since the instrument was introduced in 1999. Five-year and 20-year JGB yields have also reached record highs.

This shift reflects a fundamental change in investor expectations. Markets increasingly believe that inflation inside Japan will remain elevated, forcing the Bank of Japan to continue tightening monetary policy after decades of extraordinary accommodation.

The geopolitical environment has contributed significantly to this transformation. The war involving Iran and the broader instability in global energy markets have intensified inflationary pressures throughout energy-importing economies, including Japan. Because Japan imports much of its energy supply, rising oil prices rapidly feed into transportation costs, manufacturing expenses, and consumer prices across the economy.

At the same time, Prime Minister Sanae Takaichi has pursued expansionary fiscal policies aimed at cushioning the domestic economy from rising energy costs and inflationary pressure. Her government has increased subsidies and spending programs designed to stimulate economic activity and provide relief to households facing higher living expenses.

However, this combination of higher government spending and rising imported energy costs has reinforced inflationary pressures rather than reducing them. As a result, financial markets increasingly expect further Bank of Japan tightening, which in turn continues pushing Japanese bond yields higher.

This changing interest-rate environment is beginning to alter the global flow of capital.

For years, the logic behind Japanese purchases of U.S. Treasuries was straightforward. Why invest heavily in Japanese bonds yielding close to zero when U.S. government bonds offered substantially higher returns? But as Japanese yields rise, the relative attractiveness of overseas investments begins to diminish.

Japanese investors are now reconsidering whether they still need to assume currency risk, geopolitical uncertainty, and foreign-market exposure in order to achieve acceptable returns. Domestic Japanese bonds are increasingly becoming competitive alternatives to U.S. debt.

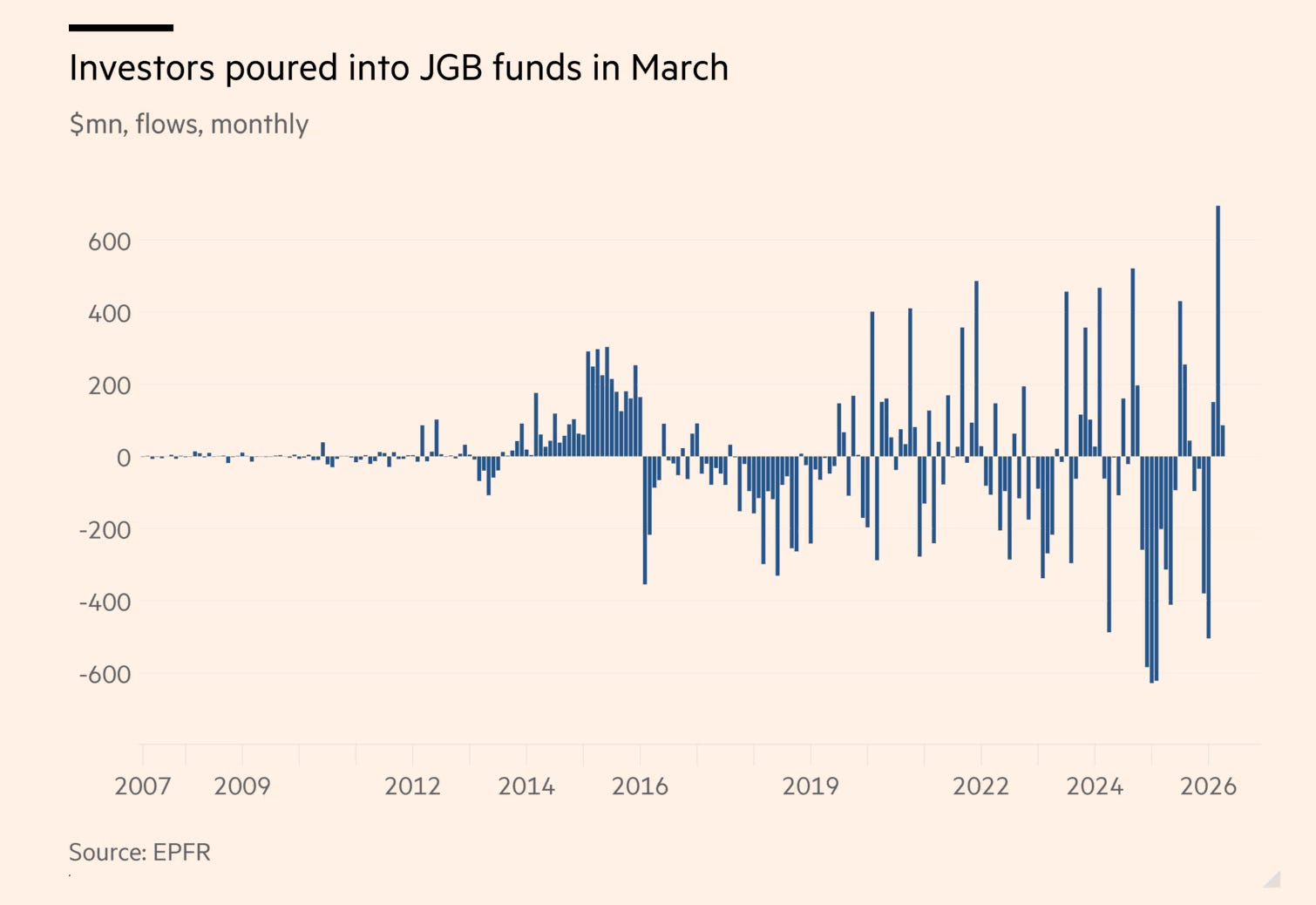

There are already signs that this transition may be underway. Investment data reportedly showed the largest monthly inflow ever into Japanese sovereign bond funds during March, suggesting that capital is beginning to rotate back into domestic markets. Mark Dowding, chief investment officer at BlueBay Asset Management, told the Financial Times that newly invested money would increasingly remain inside Japan rather than flowing into U.S. Treasuries or American corporate debt.

Such comments highlight the potentially historic scale of the shift now developing in global capital markets.

For the United States, the timing could hardly be worse.

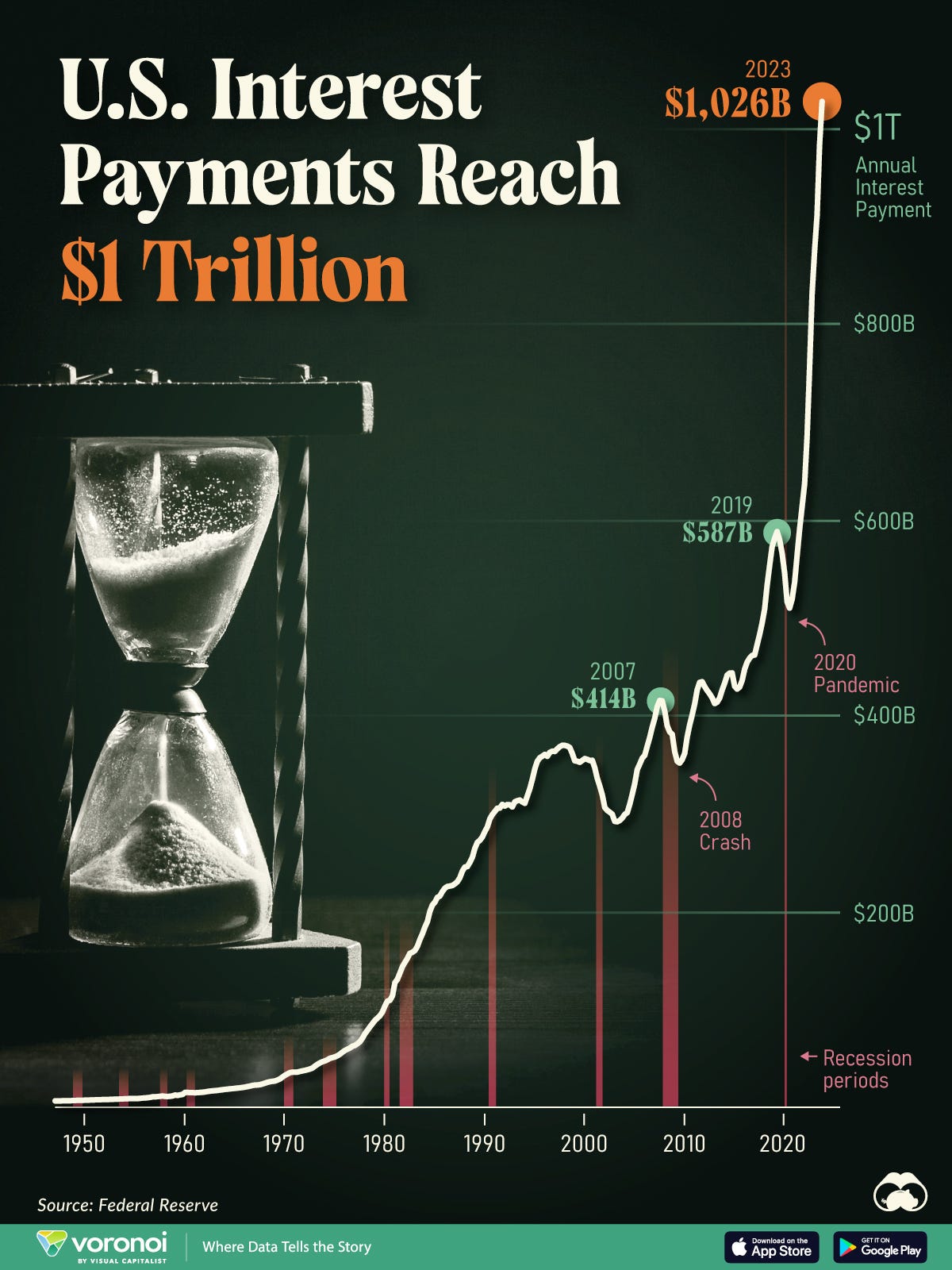

The federal government is already running extremely large deficits while simultaneously facing rapidly rising interest expenses on the national debt. Interest payments alone are approaching roughly $1 trillion annually, making debt servicing one of the fastest-growing components of federal spending.

If foreign demand for Treasuries weakens materially, the Treasury Department may be forced to offer significantly higher yields in order to attract buyers. There are already indications that this process may have started.

Several recent Treasury auctions have shown weaker-than-expected demand, particularly for longer-duration bonds. In a historically significant development, the Treasury Department recently sold $25 billion worth of 30-year Treasury bonds at a yield of approximately 5 percent — the first time since 2007 that long-term U.S. government debt reached such levels. Prior to this recent period, 30-year Treasury yields had rarely exceeded 4.75 percent in the modern era.

What makes the situation especially striking is the speed with which investor sentiment has deteriorated. Earlier this year, before the escalation of military tensions involving Iran, demand for long-duration Treasuries remained exceptionally strong. Within only a few months, however, investor caution intensified sharply as concerns surrounding inflation, deficits, geopolitical instability, and debt sustainability began converging simultaneously.

Bond investors are increasingly confronting several major risks at once.

Inflation in the United States remains persistent despite the Federal Reserve’s tightening efforts. Budget deficits continue to expand rapidly due to rising government spending and higher interest costs. Geopolitical tensions are increasing uncertainty throughout global markets. At the same time, foreign central banks that once played stabilizing roles in the Treasury market have gradually reduced their participation.

Compounding these pressures is the enormous volume of corporate debt issuance now entering financial markets. Large corporations are borrowing aggressively as well, creating direct competition between government debt and private-sector debt for investor capital. This competition places additional upward pressure on yields throughout the financial system.

The danger for Washington is that rising yields can create a self-reinforcing cycle.

As Treasury yields rise, the government’s borrowing costs increase. Higher interest payments then expand budget deficits even further. Larger deficits require additional debt issuance, which can place still more upward pressure on interest rates. Over time, this feedback loop becomes increasingly difficult to stabilize.

The Treasury Department has already indicated that it expects borrowing needs to exceed previous projections because government cash flows have weakened relative to expectations. For many analysts, this signals that debt issuance will continue expanding substantially in the years ahead.

Under normal circumstances, strong foreign demand might help absorb this growing supply of debt. But if Japanese investors increasingly repatriate capital back into domestic markets, one of the most important sources of foreign demand for Treasuries could gradually weaken.

This does not necessarily imply an immediate collapse of the Treasury market or the dollar system. U.S. Treasuries remain among the deepest and most liquid financial assets in the world. Moreover, global investors often continue buying Treasuries during periods of crisis because of the absence of obvious alternatives.

Nevertheless, the structural trends now emerging may represent the early stages of a broader transformation in the global financial order.

For decades, the United States benefited from an international system in which foreign governments and investors consistently recycled surplus capital into American financial markets. Japan played a central role in sustaining that arrangement. But as Japanese yields rise and domestic investment opportunities improve, the incentives underpinning those capital flows are beginning to change.

If the world’s largest foreign holder of U.S. debt steadily redirects capital back home, the implications for Washington, Wall Street, and the broader global economy could become enormous. In highly leveraged financial systems, rising borrowing costs tend to spread rapidly across governments, corporations, banks, housing markets, and consumers alike.

The era of virtually unlimited foreign appetite for U.S. debt may not be ending overnight. But the foundations supporting that system appear increasingly unstable. And Japan’s bond market transformation may ultimately prove to be one of the most consequential financial turning points of the decade.

I discuss this topic further in a recent video:

Follow Lena Petrova:

YouTube: https://www.youtube.com/@lenapetrova

X/ Twitter: https://x.com/LenaPetrovaOnX

To continue my independent journalism, I depend on the generosity and support of my readers. This site is fully reader-supported, and I am very grateful to the readers. If you’d like to support me directly, you can do so by becoming a paid subscriber or making a one-time donation. Thank you for your continued support!

I fully expect the global economic situation to crater within the next few years. It's not sustainable anymore and something has to give. If Japan can't hang on, the rest of the western world will crumble like dominoes when Japan's economy collapses. When that happens, China and Russia will be on the sidelines telling each other, "See, I told you so."

I keep thinking that China, for all of it's faults, may be a safer bet for a stable standard of living when the house of cards finally falls down.

Japanese bonds hardly have much to commend them. The National Debt to GDP in Japan is 200%+ and rising. The US isn't great, but we are a clean shirt considering how crazy the Bank of Japan has been. They even bought Japanese stocks and suppressed interest rates for decades. Anyone who would consider tucking his money away for 30 years at 4% (Japan) or 5% (US) is absolutely clueless. I cannot imagine loaning my money to the government for 10 years, locking in an interest rate. I feel sure inflation in the US will be less than Japan's, so their money in Yen will be eroded faster than the Dollar.

For comparison purposes, Russia's National Debt to GDP is . . . 19%! How amazing is that. A responsible government, at war even, and still keeping their National Debt tiny. My hat is off to them. The Ruble may be last fiat currency standing, at that rate.